Philosophy

Investment Philosophy

Navigating Your Financial Future with Confidence

Our Philosophy

In a world of complex and ever-changing financial markets, we understand the challenges investors face. That’s why we’ve dedicated ourselves to creating a smarter, more resilient approach to investing. Our mission is to help you navigate your financial future with confidence.

Navigating Financial Markets with a Smarter Approach

At Omega Squared, our mission is to empower investors to achieve their financial goals through a disciplined, data-driven investment approach that prioritizes risk management and capital preservation. We believe that successful investing requires a deep understanding of macroeconomic trends, a commitment to quantitative analysis, and a relentless focus on delivering client-centric solutions.

Our investment philosophy is guided by three core principles:

Risk Management First

We recognize that protecting your capital is paramount to long-term success. Our strategies are designed to mitigate downside risk and navigate market volatility with resilience.

Data-Driven Decisions

We rely on rigorous research and quantitative analysis to inform our investment decisions, eliminating emotional biases and ensuring a disciplined approach.

Harnessing Macroeconomic Insights

We believe that understanding the broader economic landscape is crucial for identifying attractive investment opportunities and managing risk effectively.

Smart Alpha: Our Unique Investment Approach

At the heart of our investment philosophy is Smart Alpha, our proprietary factor-based strategy that seamlessly integrates macroeconomic analysis with tactical asset allocation. This innovative approach sets us apart by offering a more comprehensive and adaptable framework for navigating complex financial markets.

What makes Smart Alpha unique?

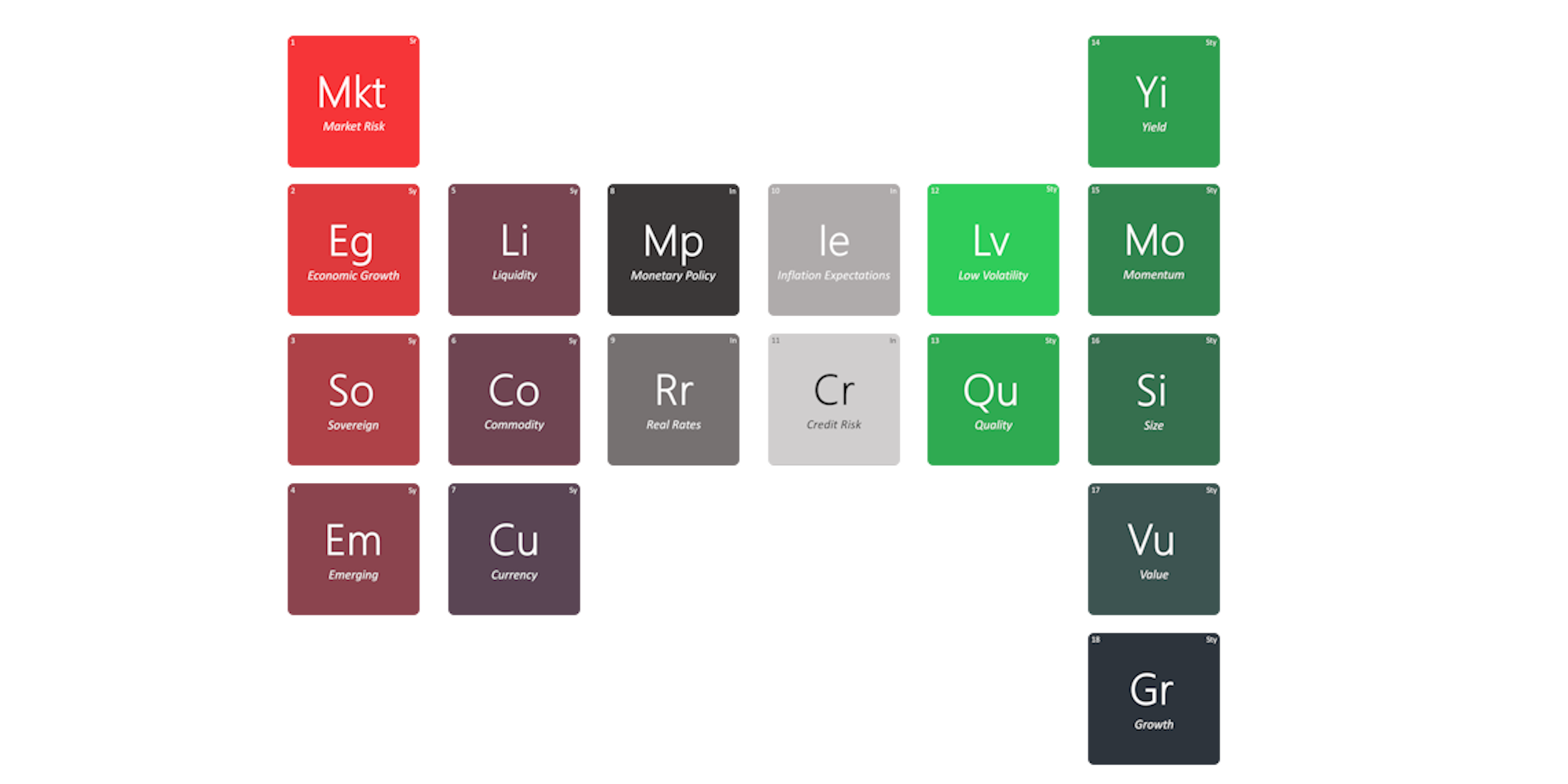

Multi-Dimensional Analysis: We combine secular analysis, business cycle classification, and factor investing to create a holistic view of the investment landscape.

Dynamic Risk Management: We actively adjust our portfolio allocations based on the prevailing economic environment and business cycle phase, ensuring that your investments are aligned with the current market conditions.

Data-Driven Insights: We leverage cutting-edge quantitative models and machine learning algorithms to identify key macroeconomic factors and anticipate market shifts, allowing us to make informed decisions with precision. Our Smart Alpha model not only identifies these key factors but also uses them to optimize portfolios for specific economic regimes. We understand that different market conditions call for different investment strategies, and we tailor our approach accordingly.

Our Smart Alpha model not only identifies key macroeconomic factors but also uses them to optimize portfolios for specific economic regimes. We understand that different market conditions call for different investment strategies, and we tailor our approach accordingly. By integrating secular analysis, business cycle classification, and factor investing, we gain a comprehensive understanding of the investment landscape and its potential risks and rewards. We then use this knowledge to dynamically adjust portfolio allocations, seeking to maximize returns while managing risk effectively. This data-driven approach ensures that your investments are always aligned with the current economic environment, giving you the best chance to achieve your financial goals.

Risk Management: The Cornerstone of Our Philosophy

Omega Squared recognizes that downside risk poses a greater threat to long-term investment success than upside potential. A significant loss requires a disproportionately larger gain to recover, making risk mitigation a top priority.

We understand that investors are inherently loss averse, and we share this perspective. Our investment strategies are designed to protect your capital during market downturns, ensuring that you can participate fully in the upside potential when the market recovers.

To achieve this, we employ a range of risk management strategies, including:

- Diversification: We strategically allocate assets across different classes and factors to reduce overall portfolio volatility.

- Tactical Asset Allocation: We adjust our portfolio's exposure to various asset classes based on our assessment of the business cycle, seeking to reduce risk during economic contractions and capture opportunities during expansions.

- Hedging Strategies: We may utilize hedging techniques to further mitigate specific risks, such as interest rate fluctuations or geopolitical events.

One of our key risk management strategies involves adjusting portfolio allocations based on the prevailing macroeconomic environment. During periods of economic expansion, we may increase exposure to assets that typically thrive in such conditions, such as equities. Conversely, during economic contractions or periods of heightened risk, we may shift towards more defensive assets like fixed income or alternative investments.

Macroeconomic Insights: Guiding Our Investment Decisions

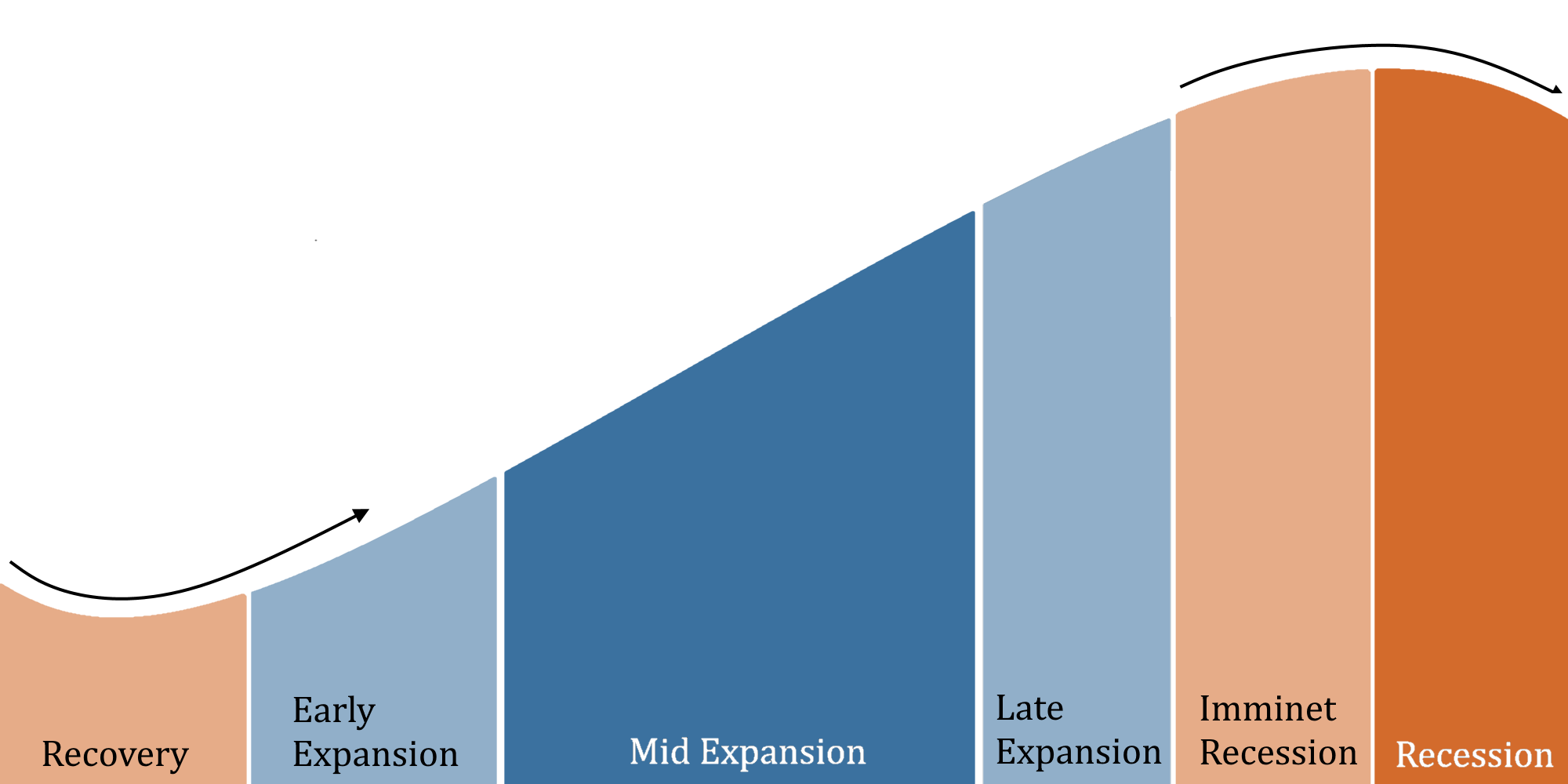

At Omega Squared, we believe that a deep understanding of macroeconomic trends is essential for making informed investment decisions. We have developed a proprietary model that classifies the business cycle into distinct stages, each with unique characteristics and investment implications. By identifying the current stage of the cycle, we can anticipate potential market shifts and adjust our portfolios accordingly.

Our research has shown that different macroeconomic regimes offer varying risk-reward relationships. By analyzing historical and current risk premia, we can identify assets and factors that are likely to outperform in the current environment, allowing us to construct portfolios that are both resilient and positioned for growth. By analyzing historical and current risk premia within the context of our business cycle model, we can identify assets and factors that are likely to outperform in the current environment. This allows us to dynamically optimize portfolios to maximize returns while managing risk effectively.

Client-Centric Solutions: Tailored to Your Needs

Omega Squared is committed to delivering personalized investment solutions that align with your unique financial goals and risk tolerance. We understand that every investor is different, and we take a collaborative approach to build portfolios that meet your specific needs.

We believe that a static portfolio is not sufficient in today’s dynamic market environment. Our Smart Alpha approach allows us to actively manage your portfolio, adjusting it in response to changing macroeconomic conditions to help you achieve your investment goals.

Whether you are a high-net-worth individual, a family office, or an institutional investor, we offer a range of investment strategies tailored to your risk profile and investment objectives. Our team of experienced professionals is dedicated to providing you with the highest level of service and support.

Request an Appointment

In 15 minutes we can get to know you – your situation, goals and needs – then connect you with an advisor committed to helping you pursue true wealth.